September 30, 2026 marks the critical deadline when most UAE businesses must complete their corporate tax filing in UAE. Companies with December 31 year-ends face this approaching deadline with just seven months remaining as of February 2026.

The Federal Tax Authority emphasized in September 2025 that all Taxable Persons subject to Corporate Tax must submit their Tax Returns and settle Corporate Tax Payable within a maximum of nine months from the end of their relevant Tax Period (FTA News, September 14, 2025). Late submission triggers administrative penalties of AED 500 for each month during the first twelve months, increasing to AED 1,000 per month from the thirteenth month onwards.

Many business owners mistakenly believe corporate tax filing in UAE represents a simple annual submission similar to VAT returns. Reality proves far more complex. Audited financial statements, transfer pricing documentation, substance requirements for Free Zone entities, and detailed profit calculations demand months of preparation rather than last-minute scrambling.

This guide provides a structured preparation timeline ensuring your business approaches corporate tax filing in UAE with confidence, complete documentation, and zero deadline stress. Whether you operate a mainland company, Free Zone entity, or branch, following this roadmap prevents costly errors and compliance failures.

Author Credentials: This preparation guide was developed by Jazaa’s CFO services and tax compliance team with experience supporting UAE businesses through corporate tax registration, filing, and ongoing compliance. Our team includes CPA-qualified accountants who have processed corporate tax returns during filing cycles, tax advisors familiar with FTA requirements and audit procedures, and financial consultants who structure tax-efficient business operations across mainland and Free Zone entities.

For comprehensive accounting and tax support, visit Jazaa’s accounting services.

Scope of This Guidance: This article provides general information about preparing for corporate tax filing in UAE with focus on the September 30, 2026 deadline for December 31 year-end businesses. It addresses Federal Decree-Law No. 47 of 2022 requirements applicable to taxable persons operating in mainland UAE and Free Zones.

For specific advice tailored to your company’s tax structure, filing obligations, and compliance circumstances, consultation with qualified tax advisors familiar with FTA requirements and your individual situation is recommended.

Understanding Your Corporate Tax Filing Deadline in UAE

Corporate tax filing in UAE deadlines vary based on your company’s tax period selection during initial registration. Understanding your specific deadline prevents last-minute panic and potential penalties.

Standard Nine-Month Rule

The Federal Tax Authority requires businesses to submit corporate tax returns within nine months following their tax period end. According to Federal Decree-Law No. 47 of 2022, Article 53(1), a Taxable Person must submit a Tax Return and pay any Corporate Tax due to the FTA within 9 months of the end of its Tax Period (FTA Tax Returns Guide CTGTXR1, November 2024, page 20).

Companies selecting calendar year (December 31 year-end) must file by September 30 of the following year. For example, businesses with tax periods ending December 31, 2025 face September 30, 2026 filing deadlines. This nine-month window provides time for financial statement preparation, audit completion, and return compilation, but only when businesses start early.

Your Tax Period Determines Everything

Corporate tax filing in UAE obligations depend entirely on the tax period you selected during FTA registration. Most businesses chose calendar year alignment (January 1 to December 31) matching their financial year, but some selected different periods based on business cycles or parent company requirements.

Check your FTA corporate tax certificate showing your designated tax period. This certificate arrived when you completed registration and clearly states your first tax period dates. The Corporate Tax Law applies to Tax Periods commencing on or after 1 June 2023, and the Tax Period for the Taxable Person is the Financial Year or part thereof for which a Tax Return is required to be filed (FTA News, August 13, 2024).

First Filing vs Second Filing Considerations

Businesses filing their second returns in September 2026 benefit from previous year experience but face heightened scrutiny. FTA reviews second filings more carefully, comparing figures between years and investigating significant changes. Consistency in accounting methods and documented explanations for material variances become critical.

Special Deadlines and Extensions

FTA issued special provisions through Decision No. 7 of 2024 for businesses incorporated during specific periods, offering extended first-filing deadlines. Companies established after certain dates could receive penalty waivers if they filed within seven months of their first tax period end (FTA Decision No. 7 of 2024).

However, these special provisions apply primarily to first-time filers. Businesses approaching their second filing in September 2026 must adhere strictly to the nine-month standard deadline without extensions unless exceptional circumstances warrant formal FTA requests.

The Real Deadline: Much Earlier Than September 30

While corporate tax filing in UAE technically allows submission until September 30, practical considerations demand much earlier completion. Audited financial statements require 4-6 weeks minimum. Tax return preparation needs 2-3 weeks. Technical review and error correction adds another week.

Start your preparation process no later than March 2026 for September deadline, allowing sufficient time for each phase without rushing critical components or compromising accuracy. Jazaa’s tax planning services help businesses establish preparation timelines aligned with their specific filing deadlines and compliance requirements.

Actionable Takeaway: Corporate tax filing in UAE deadlines fall nine months after your tax period end. September 30, 2026 applies for December 31, 2025 year-ends. Check your FTA certificate confirming your specific tax period. Plan backwards from deadline, allowing 6-7 months for complete preparation including audit, documentation assembly, and filing. Contact Jazaa for consultation about your preparation timeline.

Essential Documents You Need for Filing

Corporate tax filing in UAE requires comprehensive documentation supporting your return figures, financial statements, and tax calculations. Gathering these documents early prevents last-minute searches and incomplete submissions.

Audited Financial Statements (Mandatory for Most)

Taxable Persons deriving Revenue exceeding AED 50 million during the relevant Tax Period are required to prepare and maintain audited Financial Statements (FTA Determination of Taxable Income Guide CTGDTI1, July 2024). Additionally, all Qualifying Free Zone Persons must prepare and maintain audited Financial Statements even if their Revenue is below AED 50 million during the relevant Tax Period (FTA Free Zone Persons Bulletin).

Your audited financial statements must include balance sheet, profit and loss statement, cash flow statement, notes to accounts, and auditor’s report. These statements must follow International Financial Reporting Standards (IFRS) or IFRS for SMEs as approved by FTA per Ministerial Decision No. 114 of 2023.

Audits require 4-6 weeks minimum from document submission to final report. Start audit arrangements by April 2026 for September deadline, allowing time for auditor queries, adjustments, and final review. Jazaa’s audit support services help coordinate this process.

Tax Computation Worksheets

Corporate tax filing in UAE requires detailed tax computations reconciling accounting profit to taxable income. According to the FTA Tax Returns Guide, the starting point for determining Taxable Income is Accounting Income, which is subject to adjustments in order to determine the Taxable Income for Corporate Tax purposes per Article 20 of the Corporate Tax Law (FTA Tax Returns Guide CTGTXR1, page 24).

Common adjustments include depreciation differences (accounting vs tax), entertainment expense limitations, provisions not yet deductible, related-party transaction adjustments, and exempt income exclusions. Your tax computation provides the foundation for your final tax liability calculation.

Transfer Pricing Documentation

Businesses conducting transactions with related parties or connected persons must maintain transfer pricing documentation demonstrating arm’s length pricing. According to the FTA Transfer Pricing Guide, transfer pricing rules apply to UAE businesses that have transactions with Related Parties and Connected Persons, irrespective of whether the Related Parties or Connected Persons are located in the UAE mainland, a Free Zone or in a foreign jurisdiction (FTA Corporate Tax FAQs).

Transfer pricing files include functional analysis describing business activities, comparability analysis showing market benchmarks, method selection explaining your pricing approach, and conclusions demonstrating compliance. Free Zone entities claiming Qualifying Income exemptions face particularly strict transfer pricing scrutiny per Ministerial Decision No. 97 of 2023.

Substance Documentation (Free Zone Entities)

Free Zone companies claiming Qualifying Income exemptions must demonstrate economic substance in UAE. According to the FTA, in order to be considered a Qualifying Free Zone Person, the Free Zone Person must maintain adequate substance in the UAE, derive ‘Qualifying Income’, not have made an election to be subject to Corporate Tax at the standard rates, and comply with the transfer pricing requirements (FTA Free Zone Persons Topic Page).

Substance documentation includes evidence of adequate employees (employment contracts, payroll records, qualifications), adequate expenditure (office lease, operating costs), adequate physical assets (office photos, equipment ownership), and adequate premises (lease agreements, utility bills).

Bank Statements and Payment Records

Complete bank statements for your entire tax period verify income received and expenses paid. Corporate tax filing in UAE requires reconciliation between accounting records and actual banking activity, with FTA increasingly requesting bank statements during audits.

Maintain organized payment documentation for all significant expenses. Invoices, payment vouchers, approval records, and supplier contracts support deduction claims if FTA questions specific items.

VAT Returns (If Registered)

Your filed VAT returns provide additional verification of revenue and business activity. FTA systems cross-check corporate tax filings against VAT data, investigating discrepancies between reported VAT taxable supplies and corporate tax revenues.

Ensure your VAT compliance remains current. Outstanding VAT issues complicate corporate tax filing and trigger additional FTA scrutiny. Jazaa’s VAT compliance services help maintain consistency across all tax obligations.

Trade License and Legal Documents

Current trade license showing permitted business activities, Memorandum and Articles of Association, shareholder agreements, and certificate of incorporation support your corporate structure disclosure in tax returns.

FTA verifies that reported business activities align with licensed activities, investigating businesses claiming income from activities outside their trade license scope.

Actionable Takeaway: Corporate tax filing in UAE requires audited financial statements (mandatory for revenue exceeding AED 50 million and all Free Zone entities claiming QI exemptions), tax computation worksheets, transfer pricing documentation, substance evidence (Free Zones), complete bank statements, VAT returns, and legal entity documents. Start document assembly by March 2026, engaging auditors by April, and completing documentation reviews by July. Contact Jazaa for audit support and documentation preparation.

February to March: Initial Preparation Phase

Begin your corporate tax filing in UAE preparation immediately. February 2026 marks the ideal starting point for September deadline compliance. These initial months establish foundations preventing later complications.

Conduct Financial Records Review

Review your accounting records completeness for the full 2025 tax year. Identify missing invoices, unrecorded transactions, bank reconciliation gaps, and unexplained balance sheet items requiring resolution before audit.

Common problems discovered during this review include unreconciled bank accounts (differences between accounting records and actual bank balances), missing supplier invoices (payments made without proper documentation), revenue recognition issues (sales recorded in wrong periods), and intercompany transaction documentation gaps.

Fix these issues now rather than during audit when time pressure creates rushed corrections and potential errors. Clean accounting records expedite audit processes and prevent auditor qualification concerns.

Engage Your Audit Firm

Contact auditors in February securing engagement slots for April-May audit fieldwork. Audit firms face capacity constraints during peak season, with September corporate tax deadlines creating concentrated demand.

Discuss your business activities, any complex transactions during 2025, accounting policy changes, and expected audit timeline. Auditors provide preliminary document lists and discuss potential concerns based on your industry and business structure.

Assess Small Business Relief Eligibility

Determine whether your business qualifies for Small Business Relief (SBR) providing 0% tax treatment for revenue under AED 3 million. According to the FTA, eligible Resident Persons (natural persons and juridical persons) can elect for each Tax Period if their Revenue equals or is less than AED 3,000,000 in both the current and all previous Tax Periods (FTA Small Business Relief Topic Page).

The relief means the taxpayer is treated as not having derived any Taxable Income in the Tax Period. However, Small Business Relief will not be available to Qualifying Free Zone Persons or members of a Multinational Enterprise Group (FTA Small Business Relief Guide CTGSBR1).

If you qualify, prepare formal SBR election for inclusion in your corporate tax return. SBR does not apply automatically. You must actively elect this treatment during filing, documenting your eligibility and election.

Review Related-Party Transactions

Examine all transactions with related parties, shareholders, parent companies, sister companies, or connected persons during 2025. Related-party transaction documentation represents a common FTA audit focus area.

List all intercompany sales, purchases, service fees, interest payments, management charges, royalties, and loans. For each transaction type, document the pricing methodology, market comparisons, and business rationale supporting arm’s length treatment per Article 34 of the Corporate Tax Law.

Identify Unusual or Complex Transactions

Flag any non-routine transactions requiring special tax treatment analysis. These include asset disposals, business acquisitions, restructuring transactions, significant contract changes, or new business activity launches. Complex transactions may require specific FTA guidance or technical tax analysis.

Early identification allows time for proper tax treatment research, consultation with specialists, and documentation preparation supporting your filing positions.

Update Corporate Tax Registration

Verify your FTA registration details remain current. Business activity descriptions, contact information, authorized signatories, and tax representative appointments (if applicable) should all reflect current status. Registration changes require formal FTA notification through EmaraTax portal.

Outdated registration information creates filing complications when FTA communications reach wrong contacts or business activity mismatches trigger investigation queries.

Actionable Takeaway: Use February-March 2026 for corporate tax filing in UAE foundation work: review accounting records completeness, engage audit firms securing capacity, assess SBR eligibility (revenue under AED 3 million and not a Free Zone Person or MNE member), document related-party transactions, identify complex items, and update FTA registration. Contact Jazaa for comprehensive financial reviews and audit preparation support.

April to May: Financial Statement Finalization

Corporate tax filing in UAE depends on accurate, complete financial statements forming the foundation of your return. April-May 2026 represents critical months for finalizing these statements and commencing audit processes.

Complete Year-End Closing Procedures

Finalize all 2025 accounting entries including accruals for expenses incurred but not yet invoiced, provisions for expected costs or liabilities, depreciation calculations for fixed assets, inventory valuations at year-end, and revenue recognition adjustments ensuring proper period allocation.

Year-end closing requires careful attention to cutoff. Expenses and revenues must appear in correct periods matching when obligations arose or services were delivered, not simply when cash moved. FTA reviews cutoff procedures investigating businesses that manipulate timing for tax benefits.

Reconcile All Balance Sheet Accounts

Every balance sheet account needs reconciliation supporting the year-end balance. Account reconciliations prove balances are accurate and backed by supporting documentation.

Critical reconciliations include bank accounts (accounting balance matches bank statement), accounts receivable (listing of all customer debts owed), accounts payable (listing of all supplier amounts due), loans and borrowings (loan agreements confirming balances), and fixed assets (physical verification matching accounting records).

Auditors request reconciliations early in audit fieldwork. Completed reconciliations expedite audit processes; missing reconciliations create delays and potential audit findings.

Prepare Draft Financial Statements

Generate draft balance sheet, profit and loss statement, and cash flow statement based on your closed accounts. These draft statements form the basis for audit procedures and tax computation preparation.

Financial Statements must be a complete set of statements as specified under the Accounting Standards applied by the Taxable Person, which includes statement of income, statement of other comprehensive income, balance sheet, statement of changes in equity and cash flow statement (FTA Tax Returns Guide CTGTXR1, Glossary).

Review drafts internally identifying unusual balances, unexpected results, or items requiring explanation. Address obvious errors before submitting statements to auditors, preventing wasted audit time on correctable mistakes.

Begin Audit Fieldwork

Submit required documents to auditors and commence fieldwork during April-May allowing 4-6 weeks for completion. Audit fieldwork includes document review, transaction testing, analytical procedures, management inquiries, and specific procedures targeting risk areas.

Respond promptly to auditor queries and document requests. Delayed responses extend audit timelines, potentially missing completion targets and creating September deadline pressure.

Auditors may identify adjustments requiring accounting corrections. Evaluate proposed adjustments carefully. Material errors need correction, but minor differences may not justify financial statement changes depending on materiality thresholds.

Document Significant Accounting Policies

Prepare written descriptions of significant accounting policies applied in your financial statements. These include revenue recognition methods, expense classification approaches, depreciation policies, inventory valuation methods, and foreign currency translation treatments.

Ministerial Decision No. 114 of 2023 specifies that the only Accounting Standards accepted in the UAE for Corporate Tax purposes are the International Financial Reporting Standards (IFRS) and the International Financial Reporting Standard for small and medium-sized entities (IFRS for SMEs) (FTA Accounting Standards Guide CTGACS1).

FTA requires consistent accounting policy application across years. Policy changes require disclosure and justification. Document your policies supporting both audit requirements and future tax compliance.

Address Prior Year Comparatives

Ensure 2024 comparative figures in your 2025 financial statements match your previously filed 2024 statements. Comparative figure changes require detailed explanation and disclosure notes describing restatement reasons.

Auditors scrutinize comparative figures investigating unexplained changes. Consistent presentation between years prevents questions and demonstrates reliable financial reporting.

Actionable Takeaway: Use April-May 2026 to finalize corporate tax filing in UAE financial statements: complete year-end entries, reconcile all balance sheet accounts, prepare draft statements following IFRS or IFRS for SMEs, commence audit fieldwork allowing 4-6 weeks, document accounting policies, and verify comparative figures. Contact Jazaa for financial reporting services and audit coordination.

June to July: Audit Completion and Documentation Assembly

Corporate tax filing in UAE requires audited financial statements finalized and comprehensive documentation assembled during June-July 2026. These months represent your critical preparation phase before actual filing begins.

Finalize Audited Financial Statements

Work with auditors resolving any remaining queries, finalizing proposed adjustments, and obtaining final audited financial statements including auditor’s report. Auditor’s report opinions matter significantly. Unqualified opinions demonstrate clean financials, while qualified opinions or disclaimers trigger FTA scrutiny.

Review audited statements carefully before acceptance. Check that all figures reconcile with underlying accounting records, notes disclosure adequately explains significant items, comparative figures match prior year, and accounting policies align with your actual practices.

Prepare Tax Computation and Reconciliation

Develop detailed tax computation reconciling accounting profit to taxable income. Start with profit from audited financial statements, then systematically add back non-deductible expenses and subtract exempt income or allowable deductions not reflected in accounting profit.

Common adjustments in corporate tax filing in UAE include:

Add back (non-deductible):

Depreciation exceeding tax depreciation allowances, entertainment expenses beyond permitted limits, penalties and fines (non-deductible per Article 33 of Corporate Tax Law), non-business expenses (personal use items), provisions not yet meeting tax deductibility rules, and related-party payments not at arm’s length.

Subtract (exempt or adjustable):

Qualifying Free Zone income (if eligible per Article 18 of Corporate Tax Law), exempt dividends received from UAE resident companies per Article 22, tax-deductible donations to approved charities per Article 32, and adjustments for timing differences.

Document each adjustment with supporting rationale and calculation backup. FTA reviews tax computations carefully, investigating inadequately supported adjustments.

Complete Transfer Pricing Documentation

Finalize transfer pricing files for all related-party transactions. Transfer pricing documentation requirements per Ministerial Decision No. 97 of 2023 include:

Functional analysis describing business functions, assets used, and risks assumed by your company and related parties. Comparability analysis identifying comparable independent transactions and companies as pricing benchmarks. Transfer pricing method selection explaining approach (Comparable Uncontrolled Price, Resale Price, Cost Plus, etc.). Documentation of pricing policies, agreements, and determinations. Financial analysis demonstrating your pricing yields arm’s length results.

Free Zone entities face heightened transfer pricing scrutiny when claiming Qualifying Income exemptions. Inadequate documentation risks FTA challenges denying Free Zone tax benefits.

Assemble Substance Evidence (Free Zones)

Free Zone companies claiming 0% tax treatment must compile comprehensive substance documentation per Article 18 of the Corporate Tax Law and Cabinet Decision No. 100 of 2023:

Employee substance:

Employment contracts showing local hire, payroll records proving UAE salary payments, immigration records (visas, labor permits), qualifications demonstrating adequate expertise, and job descriptions showing genuine responsibilities.

Asset substance:

Office lease agreements, utility bills (DEWA, internet, phone), office photos with date stamps, equipment purchase records, and IT infrastructure documentation.

Activity substance:

Meeting minutes demonstrating UAE decision-making, business correspondence showing UAE operations, customer contracts signed in UAE, project delivery evidence from UAE, and marketing activities conducted locally.

Substance failures represent significant FTA challenge areas. Comprehensive documentation prevents costly disputes and potential qualification denials.

Organize Supporting Documentation

Create organized documentation packages for potential FTA queries:

All supplier invoices for significant expenses, customer contracts supporting revenue recognition, banking records reconciled to accounting, asset purchase documentation, loan agreements and financing documents, shareholder agreements, and board meeting minutes for significant decisions.

Digital organization enables quick responses to FTA information requests during and after filing. Disorganized records delay responses and frustrate FTA officers reviewing your submission.

Conduct Internal Pre-Filing Review

Perform internal review of your complete filing package before submission. Pre-filing review checklist:

Audited financial statements complete with unqualified opinion confirmed. Tax computation reconciles to accounting profit verified. All adjustments documented with supporting rationale. Transfer pricing files complete for related transactions. Substance evidence compiled (if Free Zone claiming QI). Revenue figures match VAT returns (if registered). Prior year comparatives consistent. SBR election documented (if applicable). Supporting documentation organized and accessible.

Catching errors during internal review prevents submission mistakes requiring amendment filings and potential penalties.

Actionable Takeaway: Use June-July 2026 for corporate tax filing in UAE completion: finalize audited statements, prepare detailed tax computations reconciling accounting to taxable income, complete transfer pricing documentation per Ministerial Decision No. 97 of 2023, compile substance evidence (Free Zones) per Cabinet Decision No. 100 of 2023, organize supporting documents, and conduct internal pre-filing review. Contact Jazaa for comprehensive filing package preparation.

August: Pre-Filing Review and Calculation Verification

August 2026 represents your final preparation month before corporate tax filing in UAE submission. Use this month for thorough verification preventing errors that create amendment requirements or penalties.

Verify Tax Liability Calculations

Double-check your final tax liability calculation ensuring mathematical accuracy:

- Start with taxable income from your tax computation

- Apply AED 375,000 zero-rate threshold (first AED 375,000 taxed at 0% per Article 3 of Corporate Tax Law)

- Calculate 9% tax on remaining taxable income

- Subtract any applicable tax credits or relief amounts

- Confirm final tax payable figure

Example calculation:

Taxable income: AED 500,000

First AED 375,000: AED 0 tax (0% rate)

Remaining AED 125,000: AED 11,250 tax (9% rate)

Total tax liability: AED 11,250

The FTA General Corporate Tax Guide confirms this calculation approach: “The first AED 375,000 of Taxable Income will be subject to Corporate Tax at 0%” (FTA General Corporate Tax Guide CTGGCT1).

Review Small Business Relief Election

If electing Small Business Relief, verify you meet all eligibility criteria:

Revenue below AED 3 million for tax period confirmed. No prior election made to exit SBR verified. Proper documentation supporting revenue calculation prepared. Formal election included in return confirmed. Not a Qualifying Free Zone Person verified. Not a member of MNE Group verified.

SBR reduces your taxable income to zero regardless of actual profit, resulting in AED 0 tax liability. However, you must still file complete corporate tax return. SBR does not eliminate filing obligations, only tax payment.

Cross-Check Against VAT Returns

Compare corporate tax revenue figures against your filed VAT returns for corresponding periods. FTA systems automatically flag significant discrepancies triggering investigation queries.

Legitimate differences occur (corporate tax includes exempt supplies, different accounting methods), but material variances need documented explanations prepared in advance of FTA questions.

Confirm EmaraTax Portal Access

Verify your EmaraTax portal access functions properly. Test login credentials, confirm authorized signatories have system access, and check that your corporate tax registration appears correctly in the portal.

The FTA highlighted that Corporate Tax registration is available through the EmaraTax digital tax services platform, launched as part of the FTA’s comprehensive digital transformation strategy (FTA News, September 14, 2025).

Technical access issues discovered in September create unnecessary deadline pressure. Resolve portal problems in August allowing time for FTA technical support assistance if needed.

Prepare Payment Arrangements

Calculate your final tax payment amount and ensure sufficient funds availability. Corporate tax payment occurs through EmaraTax portal during filing, requiring immediate payment capability.

Companies anticipating large tax liabilities should arrange financing or cash flow planning ensuring payment capacity. Late payment triggers administrative penalties per Cabinet Decision No. 75 of 2023 even if return filing occurs on time.

Review Filing Instructions and Updates

Check FTA website for any updated corporate tax filing instructions, technical guidance, or clarifications issued during 2026. Filing requirements evolve based on FTA experience and taxpayer questions.

The FTA called on all Taxable Persons to review the Corporate Tax Law, along with all related legislation including Cabinet Decisions, Ministerial Decisions, FTA Decisions, guides and public clarifications issued by the FTA, available on the FTA’s official website (FTA News, September 14, 2025).

Conduct Dry Run Filing Review

Perform mock filing review walking through EmaraTax portal screens without actual submission. Dry run review identifies:

Required data fields you have not prepared, document upload format requirements, calculation screens requiring specific breakdowns, disclosure requirements you overlooked, and technical submission requirements.

Discovering these issues in August allows correction time rather than discovering problems during September when deadline pressure creates stress.

Engage Professional Review (If Needed)

Consider engaging tax professionals for independent filing review if your business has complex transactions, significant tax liability, or uncertainty about filing positions. Professional review provides quality assurance and identifies potential issues before FTA review.

External review cost proves minimal compared to penalties, interest, and professional fees resolving FTA disputes from filing errors.

Actionable Takeaway: Use August 2026 for final corporate tax filing in UAE verification: double-check tax calculations using AED 375,000 threshold plus 9% rate, review SBR elections against eligibility criteria, cross-check against VAT returns, confirm portal access, arrange payment funds, review updated FTA guidance, conduct dry run filing, and consider professional review for complex situations. Contact Jazaa for independent filing review services.

September: Filing Submission and Payment

September 2026 marks actual corporate tax filing in UAE submission month. Following proper submission procedures ensures accurate filing without technical errors or deadline violations.

Plan Submission Timing

Avoid September 30 deadline rush. Submit your return by mid-September providing buffer for technical issues, error corrections, or portal problems. FTA systems face high traffic near deadlines, potentially creating access difficulties.

Target September 15 submission allowing two weeks for problem resolution if issues arise. This buffer protects against technical problems, last-minute questions, or unexpected complications.

Access EmaraTax Portal

Log into EmaraTax portal using authorized user credentials. Navigate to corporate tax section and select “File Tax Return” option for your relevant tax period.

The EmaraTax platform is continuously updated and enables users to complete tax procedures easily and transparently, 24/7, including Corporate Tax registration, filing of Tax Returns, settling of Corporate Tax Payable, and other tax-related services (FTA News, September 14, 2025).

Ensure you are filing for correct tax period. Verify the dates shown match your intended filing period before proceeding. Filing for wrong periods creates complications requiring amendment submissions.

Complete Return Sections Systematically

Work through corporate tax return sections methodically. The FTA Tax Returns Guide explains that a Tax Return comprises several parts allowing a Taxable Person to report their Taxable Income including any relevant adjustments, such as exemptions and reliefs claimed (FTA Tax Returns Guide CTGTXR1, page 20):

Part A: Taxable Person Information

Verify registration details display correctly, confirm tax period dates match your filing period, and check contact information currency.

Part B: Elections

Enter applicable elections including Small Business Relief, realisation basis, transitional rules, and other relief elections.

Part C: Accounting Schedule

Upload audited financial statements in required format (typically PDF), enter key balance sheet and P&L figures in portal fields, and attach auditor’s report.

Part D: Accounting Adjustments and Exempt Income

Enter accounting profit from financial statements, detail each adjustment adding or subtracting from accounting profit, and calculate final taxable income.

Part E: Reliefs

Claim Qualifying Group relief, Business Restructuring Relief, or other applicable reliefs with supporting documentation.

Part F: Other Adjustments

Enter non-deductible expenditure adjustments, interest expenditure adjustments per Article 30, and related party transaction adjustments.

Part G: Tax Liability and Tax Credits

Apply tax rates and calculate liability, claim any Foreign Tax Credits, and determine final Corporate Tax Payable.

Part H: Review and Declaration

Review all entries and complete declaration confirming accuracy.

Part I: Schedules

Complete required schedules based on your circumstances (Free Zone, Tax Group, Transfer Pricing, etc.).

Upload Supporting Documents

Corporate tax filing in UAE requires uploading supporting documentation:

Audited financial statements (mandatory), tax computation worksheets, transfer pricing documentation (if related transactions), substance evidence (if Free Zone claiming QI), and other supporting schedules or analyses.

Ensure document files meet FTA format and size requirements. Large file uploads may require compression or splitting into multiple files.

Review and Validate Submission

Before final submission, use portal validation tools checking for:

Mathematical errors in calculations, missing required fields, incomplete sections, document upload confirmation, and consistency checks between sections.

Portal validation catches common errors preventing submission of obviously incorrect returns requiring later amendment.

Submit Return and Process Payment

After validation confirmation, submit your corporate tax return. Portal generates payment screen showing tax liability due. Process payment immediately through portal using:

Direct bank transfer, authorized payment service providers, or corporate credit facilities (if established).

The FTA advises all Corporate Taxable Persons to verify their Tax Periods based on their Financial Year and check the deadlines for filing returns and settling any outstanding tax liabilities (FTA News, September 24, 2025).

Payment confirmation generates upon successful processing. Save payment receipt for your records proving timely payment.

Download and Save Confirmation

Portal generates filing confirmation document after successful submission showing:

Return submission date and time, tax period filed, tax liability amount, payment confirmation, and submission reference number.

Download and save this confirmation. It proves your filing compliance if later questions arise about timing or submission.

Monitor Portal for Acknowledgment

FTA reviews filed returns generating acknowledgment typically within 2-4 weeks. Monitor your EmaraTax portal inbox for FTA communications including:

Return acceptance confirmation, information requests (if FTA has questions), assessment notices, and audit notifications.

Respond promptly to FTA information requests preventing delays or penalties for non-cooperation.

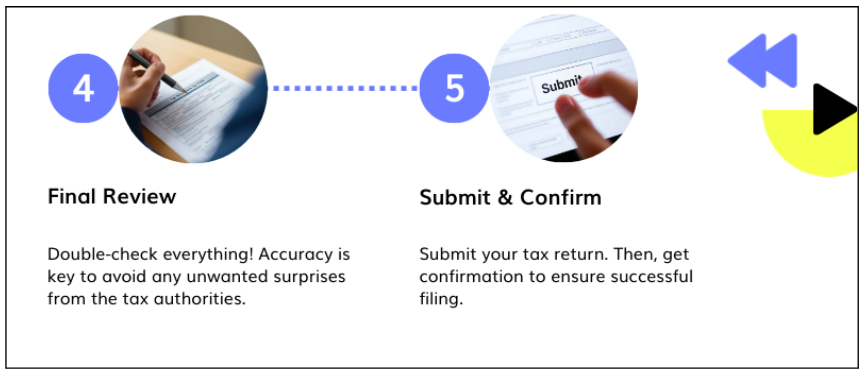

Actionable Takeaway: Complete corporate tax filing in UAE submission by mid-September 2026: access EmaraTax portal, complete return sections systematically (Parts A through I), upload supporting documents, validate submission, process payment immediately, download confirmation, and monitor portal for FTA acknowledgment. Avoid September 30 deadline rush targeting September 15 submission. Contact Jazaa for filing services and submission support.

Common Filing Mistakes and How to Avoid Them

Corporate tax filing in UAE contains common error patterns creating penalties, amendments, or FTA investigations. Understanding these mistakes enables proactive avoidance.

Mistake 1: Missing the Filing Deadline

Late filing triggers automatic penalties. The FTA clarified that late submission of a Tax Return or a delay in settling the Corporate Tax Payable will result in an administrative penalty of AED 500 for each month, or part thereof, during the first twelve months, increasing to AED 1,000 for each month from the thirteenth month onwards (FTA News, September 14, 2025).

Deadline violations occur when businesses underestimate preparation time or encounter last-minute complications.

Prevention: Start preparation in February-March, maintain detailed timeline tracking progress, and target mid-September submission rather than September 30 deadline.

Mistake 2: Filing Without Audited Financials

Many businesses submit returns without proper audited financial statements, assuming audit is not mandatory or that unaudited statements suffice. FTA rejects incomplete returns lacking required audit reports for companies meeting audit thresholds.

According to FTA guidance, Taxable Persons deriving Revenue exceeding AED 50 million and all Qualifying Free Zone Persons are required to prepare and maintain audited Financial Statements.

Prevention: Engage auditors by April allowing 4-6 weeks completion time, clarify audit requirements with FTA if uncertain, and never submit without complete audited financials unless specifically exempted.

Mistake 3: Inadequate Transfer Pricing Documentation

Related-party transactions without proper arm’s length documentation trigger FTA challenges, potential income adjustments, and penalties. Transfer pricing failures represent common audit findings.

Prevention: Document all related transactions contemporaneously, prepare formal transfer pricing studies for significant transactions, benchmark pricing against market comparables, and maintain comprehensive documentation files per Ministerial Decision No. 97 of 2023.

Mistake 4: Weak Substance Claims (Free Zones)

Free Zone entities claiming Qualifying Income exemptions without adequate substance documentation face FTA challenges denying tax benefits. Substance failures result in businesses losing expected Free Zone advantages paying full 9% tax.

Prevention: Maintain detailed substance evidence throughout the year (employee records, office documentation, activity proof), take contemporaneous photos of UAE operations, document decision-making occurring in UAE, and compile comprehensive evidence packages supporting substance claims per Cabinet Decision No. 100 of 2023.

Mistake 5: Inconsistent VAT and Corporate Tax Figures

Significant unexplained differences between VAT return revenues and corporate tax revenues trigger automated FTA flags investigating potential tax evasion. Cross-system checking catches obvious inconsistencies.

Prevention: Reconcile corporate tax revenue to VAT taxable supplies before filing, prepare written explanations for legitimate differences (exempt supplies, different recognition methods), and ensure accounting consistency across all tax filings.

Mistake 6: Incorrect Small Business Relief Application

Businesses ineligible for SBR claiming relief face penalties and interest on unpaid tax. SBR misapplication occurs when companies misunderstand revenue thresholds or eligibility rules.

Prevention: Calculate total revenue carefully including all income sources, verify eligibility criteria match your situation (under AED 3 million, not Free Zone Person, not MNE member), document revenue calculation supporting SBR claim, and consider professional review if near AED 3 million threshold.

Mistake 7: Mathematical Errors in Tax Calculations

Basic calculation mistakes occur in tax computations. Adding instead of subtracting adjustments, applying wrong tax rates, or miscalculating taxable income. Mathematical errors seem simple but create amendment requirements and potential penalties.

Prevention: Double-check all calculations independently, use spreadsheet formulas rather than manual math, have second person review computations, and use portal validation tools before submission.

Mistake 8: Disorganized or Missing Supporting Documents

FTA information requests during review require specific supporting documents. Businesses unable to provide documentation face assessment estimates, denied deductions, and penalties for inadequate record-keeping.

According to FTA guidance, Taxable Persons shall maintain all records and documents for a period of 7 years following the end of the Tax Period to which they relate.

Prevention: Maintain organized digital filing systems throughout the year, scan all significant documents immediately upon receipt, create indexed documentation packages for filing, and establish document retention policies meeting FTA seven-year requirements.

Actionable Takeaway: Common corporate tax filing in UAE mistakes include deadline violations (AED 500-1,000 monthly penalties), missing audits, weak transfer pricing, inadequate substance, VAT inconsistencies, incorrect SBR (requires under AED 3 million revenue), calculation errors, and poor documentation (seven-year retention required). Prevent errors through early preparation, professional engagement, systematic documentation, and independent review before submission. Contact Jazaa for compliance review services.

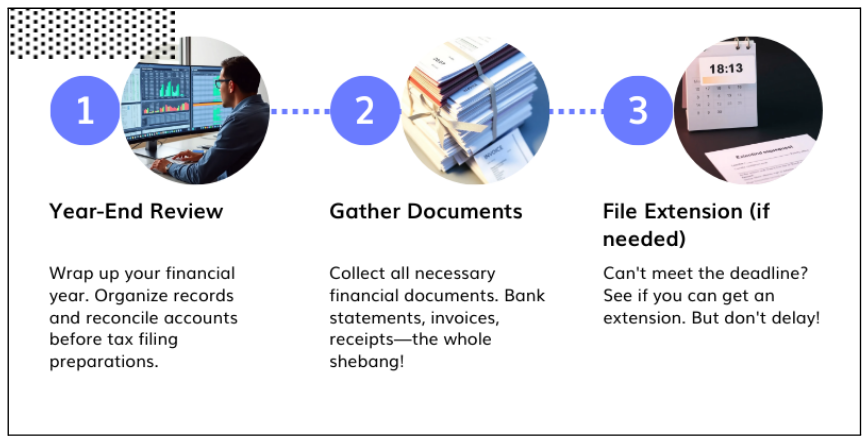

Preparation Checklist: Your Month-by-Month Timeline

Use this comprehensive checklist tracking your corporate tax filing in UAE preparation progress toward September 30, 2026 deadline:

February 2026

Review 2025 accounting records completeness. Identify and resolve recording gaps or errors. Contact audit firms for engagement discussions. Assess Small Business Relief eligibility against AED 3 million threshold. List all related-party transactions. Flag complex or unusual transactions requiring analysis. Verify FTA registration details currency.

March 2026

Complete missing accounting entries. Finalize audit firm engagement. Begin related-party documentation assembly. Initiate transfer pricing analysis if needed. Update corporate tax knowledge for 2026 requirements through FTA guides.

April 2026

Complete year-end closing procedures. Reconcile all balance sheet accounts. Prepare draft financial statements per IFRS or IFRS for SMEs. Submit documents to auditors. Begin audit fieldwork. Document significant accounting policies.

May 2026

Respond to auditor queries promptly. Address proposed audit adjustments. Finalize any required accounting corrections. Continue audit fieldwork toward completion. Verify comparative figures consistency with prior year.

June 2026

Receive final audited financial statements. Review auditor’s report for qualifications. Begin tax computation preparation reconciling accounting to taxable income. Document all tax adjustments with rationale per Corporate Tax Law articles. Finalize transfer pricing documentation per Ministerial Decision No. 97 of 2023. Compile substance evidence (if Free Zone) per Cabinet Decision No. 100 of 2023.

July 2026

Complete tax computation reconciliation applying AED 375,000 threshold. Organize all supporting documentation. Prepare SBR election documentation (if applicable and eligible). Conduct internal pre-filing review using checklist. Cross-check against VAT returns. Verify all required documents assembled.

August 2026

Double-check tax liability calculations. Confirm EmaraTax portal access working. Arrange payment funds for tax liability. Review updated FTA guidance on website. Conduct dry run filing review through portal screens. Engage professional review if needed for complex situations. Resolve any identified issues.

September 2026 (First Half)

Access EmaraTax portal with credentials. Complete return sections systematically (Parts A through I). Upload all supporting documents in required formats. Validate submission through portal tools. Submit return by September 15. Process payment immediately upon submission. Download confirmation documentation.

September 2026 (Second Half)

Monitor portal for FTA acknowledgment. Respond to any FTA information requests promptly. Save all filing confirmations. Update tax compliance records. Begin planning for next tax period.

Frequently Asked Questions

1. When is the corporate tax filing deadline for my business?

Corporate tax filing in UAE deadlines fall nine months after your tax period end. Businesses with December 31, 2025 year-ends must file by September 30, 2026. Check your FTA corporate tax certificate showing your designated tax period. This determines your specific deadline based on Article 53(1) of Federal Decree-Law No. 47 of 2022.

2. Do I need audited financial statements for corporate tax filing?

Yes, for most businesses. According to FTA guidance, Taxable Persons deriving Revenue exceeding AED 50 million during the relevant Tax Period and all Qualifying Free Zone Persons (irrespective of Revenue level) are required to prepare and maintain audited Financial Statements per Ministerial Decision No. 82 of 2023. Very small businesses below these thresholds may qualify for exemptions, but verify your specific requirements.

3. What is Small Business Relief and do I qualify?

Small Business Relief provides 0% tax treatment for Resident Persons (natural persons and juridical persons) with Revenue equal to or less than AED 3,000,000 in both the current and all previous Tax Periods (FTA Small Business Relief Topic Page). If you qualify, you must actively elect SBR in your corporate tax return. It does not apply automatically. SBR eliminates tax liability but does not eliminate filing obligations. You must still submit complete return. SBR is not available to Qualifying Free Zone Persons or members of MNE Groups.

4. What happens if I miss the September 30 deadline?

Late corporate tax filing in UAE triggers administrative penalties of AED 500 for each month, or part thereof, during the first twelve months, increasing to AED 1,000 for each month from the thirteenth month onwards (FTA News, September 14, 2025). FTA may also restrict business operations until filing compliance occurs. File immediately if you miss deadline, request penalty waiver consideration if you have legitimate reasons for delay, and engage professional assistance resolving late filing situations.

5. What is the late registration penalty for corporate tax?

If a person who must register for Corporate Tax does not submit a Tax Registration application by the applicable deadline, they will be subject to an Administrative Penalty of AED 10,000 (FTA News, January 28, 2025). This penalty applies to registration delays, separate from filing penalties.

6. How do I prove substance for Free Zone Qualifying Income?

Free Zone substance requires maintaining adequate substance in a Free Zone per Article 18 of the Corporate Tax Law. This includes evidence of adequate employees (contracts, payroll, visas), adequate expenditure (office costs, operations), adequate physical assets (office, equipment), and adequate premises (lease, utilities). Compile comprehensive documentation packages including employment records, financial evidence, office photos, activity proof, and decision-making documentation demonstrating genuine UAE operations per Cabinet Decision No. 100 of 2023.

7. Will FTA audit my corporate tax return?

FTA conducts risk-based corporate tax audits targeting returns with indicators of potential issues. These include significant related transactions, Free Zone income claims, inconsistencies with VAT, unusual tax positions, or random selection. Maintain comprehensive supporting documentation for all filing positions prepared to respond to FTA information requests. Accurate, well-documented returns reduce audit risk.

8. Can I amend my corporate tax return after submission?

Yes, if you discover errors after filing, you can submit amended corporate tax returns through EmaraTax portal. A Voluntary Disclosure is a form prepared by the FTA pursuant to which a Taxpayer notifies the FTA of an error or omission in the Tax Return per Federal Decree-Law No. 28 of 2022 on Tax Procedures (FTA Tax Returns Guide CTGTXR1, Glossary). However, amendments triggering additional tax liability incur interest charges from original due date. File amendments promptly upon discovering errors rather than waiting for FTA to identify problems.

9. How is corporate tax calculated in UAE?

Corporate Tax is imposed at 0% on the first AED 375,000 of Taxable Income and 9% on Taxable Income exceeding AED 375,000 per Article 3 of the Corporate Tax Law. For example, Taxable Income of AED 6 million results in tax liability of AED 506,250 (0% on first AED 375,000 plus 9% on remaining AED 5,625,000). Qualifying Free Zone Persons pay 0% on Qualifying Income and 9% on other Taxable Income per Article 3(2).

10. Where can I get help with corporate tax filing preparation?

Jazaa provides comprehensive corporate tax filing services including audit coordination, tax computation preparation, transfer pricing documentation, substance evidence compilation, return preparation, portal submission, and post-filing support. Contact us at jazaa.com/contact-us for consultation about your specific corporate tax filing needs and preparation timeline requirements.

Take Action Now

September 30, 2026 arrives faster than expected. Corporate tax filing in UAE requires months of preparation, not last-minute scrambling. Starting now in February 2026 provides adequate timeline for comprehensive preparation preventing deadline panic.

Following this month-by-month preparation guide ensures your business approaches filing with complete documentation, accurate calculations, and confidence in compliance. The alternative of waiting until summer creates rushed audits, incomplete documentation, and potential errors triggering penalties or FTA challenges.

Jazaa’s tax compliance services help UAE businesses navigate corporate tax filing requirements with comprehensive support from initial preparation through final submission. Our team handles audit coordination, financial statement review, tax computation preparation, transfer pricing documentation, substance evidence compilation, and portal filing ensuring accurate, timely compliance.

Do not let September deadline create unnecessary stress. Contact Jazaa today for consultation about your corporate tax filing preparation needs. We help businesses across Dubai, Abu Dhabi, and the Emirates achieve stress-free tax compliance without compromising accuracy or missing deadlines.

Actionable Takeaway: Your small business’s e-invoicing software selection should begin immediately if not already completed. Document requirements, evaluate shortlisted options through free trials, verify UAE compliance roadmaps, assess total costs including ASP fees, and plan adequate implementation timelines. For professional guidance navigating software selection, contact Jazaa’s accounting technology advisory team for independent evaluations, implementation support, and FTA compliance verification ensuring successful e-invoicing readiness before July 2027 mandatory deadlines.